The Financial Times reports that hedge funds have transformed themselves and are increasingly influencing policy.

My own work provides some empirical support for these observations. My study “Hedge Fund Manager Registration under the Dodd Frank Act” shows that hedge fund managers are only mildly affected by unprecedented registration and disclosure obligations under the Dodd-Frank Act and will be able to grow their influence in future years. This may have many significant policy implications.

Two additional empirical studies are forthcoming and should help narrow down the effects of Title IV on hedge fund managers. One study pertains to the effect of Title IV on hedge fund manager earnings (in a regression discontinuity design), the other study evaluates the effect of Title IV on smaller hedge fund advisers. Initial results are significant and have important policy implications.

Another study will evaluate the impact of the Alternative Investment Fund Managers (AIFM) Directive on the European Hedge Fund Industry.

Please see the executive summary and summary graphs for the first of these four studies (“Hedge Fund Manager Registration under the Dodd Frank Act”) below:

Executive Summary: Most hedge fund managers are not altering the size of their funds to avoid Dodd-Frank Act requirements. Managers are also not altering their investing styles. Most of the new registration and disclosure requirements have not affected the returns for hedge fund investors. Only very few managers have changed their funds’ legal structure in response to Dodd-Frank Act requirements. Rather, hedge funds are adapting to the new requirements by outsourcing compliance work, hiring additional counsel, establishing new record-keeping policies, hiring additional staff, and changing marketing materials and investor communication.

Please see the summary graphs below:

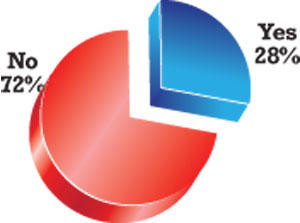

Plan a Strategic Response to Dodd-Frank

: A minority of respondents in the survey has planned a strategic response to the Dodd-Frank Act requirements. This suggests that the requirements in Dodd-Frank and the SEC regulations implementing these requirements are not perceived as materially changing the existing business and compliance model.

Plan a Strategic Response to Dodd-Frank

: A minority of respondents in the survey has planned a strategic response to the Dodd-Frank Act requirements. This suggests that the requirements in Dodd-Frank and the SEC regulations implementing these requirements are not perceived as materially changing the existing business and compliance model.

Consider Current Regulations to Determine AUM Size: A majority of respondents did not plan to change their assets under management in response to the new regulatory environment even though lowering the AUM below a certain threshold could exempt hedge fund advisers from the Dodd-Frank Act requirements.

Consider Current Regulations to Determine AUM Size: A majority of respondents did not plan to change their assets under management in response to the new regulatory environment even though lowering the AUM below a certain threshold could exempt hedge fund advisers from the Dodd-Frank Act requirements.

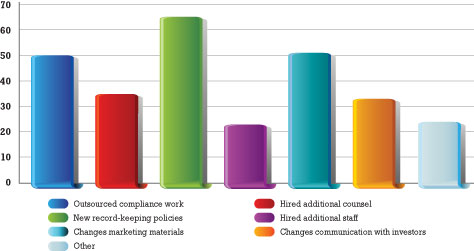

Most Common Actions Taken

: Hedge fund managers’ most common strategic responses in reaction to the registration and disclosure requirements under the Dodd-Frank Act include new record-keeping policies, the outsourcing of compliance work and changes in marketing materials. Most respondents indicated that they are addressing the requirements through compliance measures.

Most Common Actions Taken

: Hedge fund managers’ most common strategic responses in reaction to the registration and disclosure requirements under the Dodd-Frank Act include new record-keeping policies, the outsourcing of compliance work and changes in marketing materials. Most respondents indicated that they are addressing the requirements through compliance measures.

Least Common Actions Taken

: It is not common for hedge fund managers to change of the funds’ legal structure or to lower the AUM to escape the application of the Dodd-Frank Act.

Least Common Actions Taken

: It is not common for hedge fund managers to change of the funds’ legal structure or to lower the AUM to escape the application of the Dodd-Frank Act.

Take Regulatory Regime into Account for AUM: 25 per cent of respondents plan on decreasing the AUM size of their funds to avoid the regulatory hassle. Others will increase current AUM size to cover expenses.

Take Regulatory Regime into Account for AUM: 25 per cent of respondents plan on decreasing the AUM size of their funds to avoid the regulatory hassle. Others will increase current AUM size to cover expenses.

Desired AUM After Dodd-Frank Act: The ideal AUM size for most respondents is somewhere between$150 million and $1.5 billion. However, existing regulation does not appear to have influenced funds’ choice regarding the size of their AUM. Choosing a particular AUM size is based on a fund’s strategy and its existing size.

Factors Influencing AUM Preference : Title IV does not appear to have influenced fund managers’ choice regarding the size of their AUM. Choosing a particular AUM size is based on fund managers’ strategy and its existing size.

Private fund profitability after the enactment of the Dodd-Frank Act: While the new requirements do not appear to have change the earnings of hedge funds themselves, the profitability of the management company appears to be affected.

Dodd-Frank Affect Fund’s Earnings?

Dodd-Frank Affect Management Company Profits?

Dodd-Frank Affect Management Company Profits?

Cost of Compliance with Title IV: The cost of compliance for the hedge fund industry is somewhat moderate. 48 per cent of respondents did not incur more than $100,000.00 in compliance costs per year after the enactment of the Dodd-Frank Act.

Cost of Compliance with Title IV: The cost of compliance for the hedge fund industry is somewhat moderate. 48 per cent of respondents did not incur more than $100,000.00 in compliance costs per year after the enactment of the Dodd-Frank Act.

Related articles

- US Hedge Funds Threaten To Pull Back From Europe (valuewalk.com)

- Dodd-Frank act: After 3 years, a long to-do list (usatoday.com)

- Family Offices, the New Hedge Funds (cnbc.com)

- 100 Largest Hedge Funds Manage 61% Of Industry Capital (valuewalk.com)

- Hedge Funds Aren’t Crazy About The WhiteWave Foods Co (WWAV) Anymore (insidermonkey.com)

- Bank’s Lobbyists Help in Drafting Financial Bills (dealbook.nytimes.com)