By

Wulf A. Kaal & Marco Dell’Erba

Abstract

Initial Coin Offerings (ICOs) are the most efficient means of financing entrepreneurial initiatives in the history of capital formation. ICOs minimize transaction cost, democratize finance, and in the process dis-intermediate banks. Yet, ICOs have increasingly involved cases of abuse, lacking quality, and governance concerns, precipitating calls for increased regulation. This article provides an overview of the ICO market as it exists in November 2017 including the ICO process, roadmap, market conditions, crypto economics for ICO startups, core risk factors for investors and red flags of ICO practices that require industry or regulatory improvements.

Initial Coin Offerings

Initial Coin Offerings (ICOs) provide unprecedented efficiency for capital formation in startups. ICO offer liquidity enhancement of startup finance needs through crypto investors, overcoming fundraising challenges for entrepreneurial initiatives. ICOs allow crypto startups, Fintech startups, and increasingly legacy system innovators, and the Ethereum developer community, among others, to fundraise directly in the crypto community for their activities and projects, bypassing both banking and non-banking entities (i.e. VCs) as well as their services.

ICOs can be distinguished from initial public offerings (IPOs). ICOs enable the sale of a stake in a crypto project that aims to raise funds at an early stage of development. Unlike IPOs, where companies sell stocks via regulated exchange platforms, ICOs sell digital coupons, so-called presale tokens that do not generally confer ownership rights, to early investors via unregulated or exempt exchange platforms. Risks and Rewards of tokens differ from those of equity. Unlike token ownership, equity typically conveys a right to dividends. In the case of bankruptcy, equity owners have some claims on the assets of the company. Moreover, unlike IPOs, successful ICOs do not require the support of a reputable banking institution as underwriters and remove the associated fees for the issuer. ICO fundraising is substantially less expensive than traditional IPO fundraising because of the relative absence of regulatory constraints and procedures in the ICO space, in addition to simpler reporting requirements, coupled with a systematic adoption of digital identity-based processes instead of paperwork in all the phases of the process.

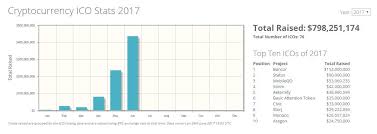

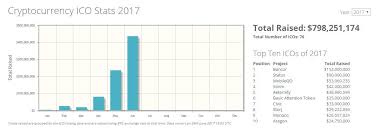

ICOs can also be distinguished from crowdfunding. Unlike crowdfunding, ICOs involve a financial stake in the company including, as the case may be, the right to vote on future decisions. Therefore, ICOs cannot be qualified as a donation. Unlike any campaigns conducted on crowdfunding sites such as Kickstarter, ICOs have often an element of a speculative purpose or a particular infrastructure use case developed on platforms and cryptocurrencies. ICOs are evolving rapidly. After Satoshi Nakamoto established the use of blockchain technology for cryptocurrencies in 2008, it took until 2012 for the first ICO. However, the exponential growth of ICOs since 2015 culminated in ICO fundraising outperforming venture capital financing of crypto startups in the second quarter of 2017. Several prominent ICOs help illustrate the rapid evolution of the ICO market. In April 2016, the startup Gnosis, a decentralized prediction platform, raised about $12.5 million in 12 minutes, skipping any venture capital firm or wealthy investor network. In May 2016, the startup Blood raised $5.5 million in 2 minutes. Brave, a start-up developing a web browser via the so-called Basic Attention Tokens, raised $35.5 million in 30 seconds. In June 2016, the Bancor Foundation collected $153 million in three hours.

Ethereum enabled a uniform protocol for the overwhelming majority of ICOs. the most significant transformation in the ICOs market to date. Ethereum’s decentralized platform incorporating smart contracts allows developers to build applications on the Ethereum blockchain. Given these advantages, the majority of developers opted for writing smart contracts on the Ethereum Virtual Machine rather than creating their own blockchain technology. Smart contracts automatically generate tokens when receiving Ether (ETH).

1. Roadmap

ICOs are a recent phenomenon that is constantly evolving. Standard market practices for ICOs change on average every quarter. Yet, a structural pattern seems to emerge. ICOs vary but often follow a timeline sequence of structural elements. Such elements are explored below:

– Before the launch of an ICO, the underlying **project is announced on cryptocurrency fora** (such as Bitcoin Talk, Cryptocointalk, Reddit).

– The announcement is followed by an **executive summary** to present the project to investors, thereby obtaining specific comments of the project.

– **Comments on the project** are considered by the management team / promoter when drafting a so-called whitepaper

– The **whitepaper** is the equivalent of an offering memorandum that provides more detailed information about the project with the purpose to support potential investors in their assessment of the project.

o Most important for the whitepaper are the key terms and the investment approach, including the investment strategy, criteria, restrictions, processes, and return so Whitepapers are not audited by any authority. Therefore these preliminary steps are crucial in order to build a general market credibility and investors’ trust in the soundness of the project

-The draft of a **yellowpaper** provides the technical specifications to support the project at this preliminary phase.

– In a first stage, in a so-called **pre-ICO **a preliminary offer is made to selected investors.

– After the signing of the offer, the **launch of the ICO is announced** and a PR campaign addressed to a broader segment of investors (typically including small investors) begins.

– After this preliminary phase, the **ICO is launched **

o The new venture sells its own cryptocurrency to be used with their software before the software itself is even written The better ICO companies may have a proof of concept or an alpha version before starting the token sale, and sometimes even a beta version as in the case of Storj.

o Funds are typically collected in Bitcoin, either via a global, public address (in which case the participants need to send Bitcoin from an address for which they control the private key) or by creating accounts of each participant and providing them with a unique Bitcoin address.

o ICO best practices suggest that all funds be held in a multi-sig address made public.

o Fundraising (usually only one) happens before the startup has launched its project, however duration of the ICOs may vary depending on the success of the entrepreneurial initiative among the investors: the most successful ICOs were concluded in a few minutes.

– The digital tokens are **listed on cryptocurrency exchanges for trading**. At the moment there are forty+ exchanges around the world that serve as secondary markets where cryptocurrencies can be traded for bitcoins in an open marketplace.

– A cryptocurrencies’ **pre-ICO price** is arbitrarily determined by the start-up team that structured the ICO, whereas the post-ICO price dynamics are determined by supply and demand. Instead of a central authority or government in ICOs the network of participants determines the price: Successful entrepreneurial activities increase the price of the tokens, granting profitable returns to investors. Should the start-up fail, the tokens’ price will plummet.

2. Market Environment

Several market factors significantly depressed fundraising for startups before the ICO market materialized in 2012 and accelerated in 2015. Banking regulation enacted in the aftermath of the financial crisis of 2008-09 affected the availability of resources for small and medium enterprises (SMEs), making fundraising for new entrepreneurial initiatives more difficult. Basel III has further increased capital requirements and risk weighted assets, resulting in a higher pressure on banks and their Return on Equity (RoE). While this led to more prudent business practices, it also significantly constrained the financing instruments available for SMEs and companies below-investment-grade. Moreover, the emergence of shadow banking, e.g. traditional banking services are provided by private investment funds, insurance companies, crowdfunding, and peer-to-peer lending, only marginally support the creation of new ventures and highly-innovative start-ups. ICOs’ rapid evolution was enabled in part by these negative factors that affected startup fundraising.

Given this market environment for startup fundraising at the inception of the ICO market, ICOs filled a void and enabled a democratization and inclusion process that facilitated banking disintermediation. ICOs allow startup to fundraise bypassing both banking and non-banking entities, e.g. VCs, as well as their services. This allows unlocking an unprecedented level of liquidity enabled by small investors who otherwise could not invest in highly innovative ventures. The Argon Group, an investment bank exclusively focused on cryptocurrencies and token-based capital markets, illustrates this trend in the evolution of investment banking services.

3. Crypto Economics

Monetary policy in crypto economics refers to the interaction of token supply, token release, and the maximum issuance of tokens in a given token issuance. An issuers’ ICOs strategy can pre-define monetary policy by predetermining the fixed number of tokens created and issued in the ICO. A maximum token issuance in combination with controlled token supply releases can result in small increases in demand driving token prices higher.

Several aspects related to the release mechanisms for tokens help manage the supply of tokens in circulation. For instance, escrow accounts can hold tokens that were not issued in the ICO. Such escrowed tokens may be released for future issuance to finance future projects of the issuer or support operational financing. To avoid a token price crash, token escrow accounts should provide usage and access controls that assure investors that escrowed tokens will not be issued at a discount. Lockups of escrowed tokens for a specified time period or phased releases can also help minimize the risks of token price crashes.

The economic benefits token holders receive from holding tokens are a key concept associated with quasi fiscal crypto policy. Two central questions help illustrate this point: 1. What is the underlying value of the issued tokens?, and 2. What factors contribute to the value appreciation or depreciation of the issued tokens? For instance, linking commercial benefits such as discounts and other benefits with token usage can incentivize token holders to use the services etc. associated with a given token. Several benefits are associated with the quasi fiscal tool of adjusting commercial benefits of tokens in crypto economics. First, the increase in commercial benefits associated with a token heightens the aggregate demand of the given token supply. Second, commercial benefits associated with a token issuance can help offset depreciated supply scarcity, e.g. the effects of a large issuance / supply of a given token in circulation. Third, commercial benefits associated with tokens can be adjusted as a form of quasi fiscal policy to control the flow of tokens in a given issuance through indirect economic incentives. Adjustments in commercial benefits can help manage operational cost changes for the issuer and the external competition with other token issuers experienced by the issuer, among other factors. Fourth, adjusting the commercial benefits associated with a given token issuance avoids more drastic monetary policy intervention by way of emergency sales or building token reserves or a decrease or increase of token supply in circulation.

To create a more significant effect, the quasi fiscal policy tool can be combined with monetary policy. If the aggregate demand for a given token issuance increases through better commercial benefits associated with the tokens, the issuer can simultaneously increase the total supply in circulation. Options for increasing the total supply of tokens in circulation include issuing escrowed tokens or even secondary issuances. The combined effect of quasi fiscal policy (increasing benefits associated with the tokens) and monetary policy (increasing the token supply in circulation) may or may not have an effect on the market price of the respective tokens. The balance of commercial benefits of a token offering and associated use cases of the token in combination with supply scarcity is critical in the issuance of a token offering.

III. Disruptive Effects

ICOs have significant disruptive effects on finance. The venture capital, startups, and banking institutions are affected by the increasing prominence of ICOs in capital formation. The reorganization of capital formation with a more efficient financing tool and crypto currencies may also affect the economy as a whole.

In particular, the ICOs disrupt the traditional business model of venture capital funds, an asset class that has traditionally played a crucial role in financing highly innovative start-ups. The disruptive effect of ICOs on the venture capital industry is in part the result of the venture capital fund lacking innovation. Paradoxically, venture capital funds continuously invested in innovation, while insufficiently innovating themselves. In the second quarter of 2017, ICO issuances exceeded venture capital financing of startups for the first time, with $210 million invested in ICOs versus $180 million invested into startups via traditional venture capital funds. This trend can be expected to continue given the superior allocation of capital at lower cost via ICOs.

ICOs display several core characteristics that make them preferable for many startups to the traditional venture capital funding model. First and foremost, ICO promoters and their developers are not forced to sacrifice their equity in the project in exchange for the funds they raised. Through borderless online sales, ICOs are directly marketed to a worldwide potential pool of investors, bypassing the typical legal, jurisdictional, and business hurdles in traditional venture capital financing. Moreover, ICOs benefit from limited accreditation standards, as well as from multiple global cryptocurrency exchanges that provide continuous access to trading with significant liquidity.

Capital formation via ICOs also disrupts the traditional hierarchies in venture capital. Traditional venture capital funds typically only allow a smaller group of elite investors to invest in highly innovative projects generally unknown to the investing public. By contrast, ICOs provide a much more inclusive option for all investors. ICOs increase the diversity and the heterogeneity of startup funding. Because of to the low barrier to entry and the borderless nature of the online token sale ICOs allow small investors from all over the world to invest.

ICOs facilitate faster capital formation for crypto startups. By contrast with traditional venture capital financing, the inclusive elements in combination with increased efficiencies, significant simplification, and better timing of capital formation provided by ICOS contributed to the creation of more liquid venture funds. Given these benefits, ICOs have the potential to disrupt other funds and asset classes including private equity and real estate funds. Given the competitive elements of ICOs, the venture capital industry is investigating ways to participate in the ICO market.

Venture capital funds increasingly try to capitalize on the opportunities presented by ICOs. The disruption of legacy finance by ICOs has triggered attempts by venture capital funds to capitalize on the source of disruption within the existing business model to benefit from its advantages. For instance, venture capital funds can capitalize on the exponential growth of cryptocurrencies. Cryptocurrencies created by blockchain startups generate investment returns that cannot be matched by legacy investments. For example, several cryptocurrencies such as Monero and NEM increase in value by 2,000%. Similarly, Ether increased by 2000% in one year, and Litecoin more than the 900%.

Venture capital funds can benefit from the early liquidity provided by cryptocurrencies. In the existing venture capital model, venture capital funds invest significant amounts of money in the hope of finding the next unicorn startup. This investment process is subject to long, complex, and time intensive processes leading up to a very late liquidity event in the form of an IPOs or acquisitions. By contrast, ICOs provide liquidity to investors much faster and allow venture capital funds to capitalize on existing profits early. Venture capital funds who invested in crypto startups gain access to much earlier liquidity via ICOs by converting their cryptocurrency profits into Bitcoin or Ether through any of the cryptocurrency exchanges and can thereafter transfer into fiat currencies via online services such as Coinsbank or Coinbase.

Blockchain Capital provides a prominent example of venture capital funds’ attempts to capitalize on the benefits associated with blockchain technology and ICOs within the VC industry. After the release of an offering memorandum on April 3, 2017, the ICO for the Blockchain Capital III Digital Liquid Venture Fund was launched on April 10. Blockchain Capital’s ICO campaign, was intended to raise 20 percent of the firm’s next fund. The ICO raised raised $10 million in in six hours, unlocking unprecedented liquidity in previously illiquid secondary venture markets. Blockchain Capital’s ICO was the first know your customer (KYC) and anti-money laundering (AML) compliant crowdsale. The entity that engaged in the ICO was incorporated in Singapore. Under applicable Regulation S and D exemptions, the ICO was able to raise money from both international and domestic investors.

In summary, ICOs’ comparative advantage over venture capital funds consists mainly of their highly cost-effective capital formation capabilities in the emerging crypto marketplaces that operates according to highly complex yet unpredictable economic dynamics. Given these ICO adnvantages, traditional regulated IPOs and venture capital funds increasingly fail to adequately capitalizing crypto and legacy ventures driven by new economic paradigms.

1. Risk Factors

Several risk factors associated with ICOs affect investors. First and foremost, the 2012 to 2017 ICO model allowed cryptocurrencies to be raised via a token sale without any conditions, landmark requirements, or security measures to protect investors. Investors’ deposit of a cryptocurrency for a crypto platform in exchange for tokens that provided a right to use the platform associated crypto product in the future did not provide such investors with any or very limited influence over how such funds were used by the ICO promoters. While most issuers typically established a form of a foundation or basic contracting to supervise promoter use of ICO proceeds, the traditional ICO model, in essence, allowed the promoters / issuer to do with the ICO proceeds as they pleased. Further limitations for token holders that amount to significant risk factors include token holders’ inability, unlike shareholders in the traditional infrastructure, to vote for or against directors or to nominate directors. While institutional investors may be able to influence the promoter decisions in the ICO pre-sale, actual ICO investors typically don’t have such influence and simply need to trust the promoters and their business intent. The only real control power for token holders is their decision to hold or sell their tokens and even that may be limited until the token is fully listed on an exchange.

Intangible or No Product

Crypto platform issuances of tokens provide an intangible or no product. During the lifecycle of a crypto platform, the platform typically starts the ICO when it has an intangible product based on a basic crypto idea but typically with no product that can be associated with such idea. Accordingly, token holders typically invest in the future promise of the idea associated with the platform. While that works well with core infrastructure products such as Ethereum, most other platforms struggle to fulfill that promise.

Associated with the lack of an existing product is the inability of most crypto platforms to generate revenue to offset costs like traditional businesses. While most crypto platform businesses in the form of a foundation may be equipped to pay their developers, crypto platforms typically do not have employees in the traditional sense that create and advertise the platform product. Similarly, while the creation of the crypto platform is associated with significant costs, crypto businesses typically do not have customers that create revenue for the business to pay for such costs. Cost associated with running a crypto platform can include the foundation itself, its developers, and the crypto marketing team, among others.

Because of the lacking product and no revenue to offset costs, ICO revenue raised by crypto platforms are often required to last for the lifecycle of the platform. Accordingly, crypto platforms are required to set aside a large number of tokens for future funding needs. Because the token supply is controlled by the ICO promoters, the token holders may be diluted in the future if the platform decides to issue more reserve tokens to additional investors. Increasing the supply of platform tokens to satisfy future funding needs and the resulting dilution because demand for the tokens decreases if supply increases means that token holder’s token value can be diminished without their ability to protect themselves against such events. The only real control token holders have to protect themselves is to sell their tokens post ICO. In fact, many venture capital funds that received tokens in exchange for their pre-ICO investments often quickly sell their tokens to protect themselves against devaluation. Other means of protection against such supply side induced devaluation of tokens can include hardcoded lockup periods for tokens. However, while such lockup periods may protect token holders against dilution, it also decreases much needed token economic flexibility for the promoter team to raise additional funds when needed.

Early Liquidity Despite Little Information Creates High Volatility

ICOs provide unprecedented liquidity without sufficient information resulting in high volatility. Unlike any prior financing vehicles, ICOs provide the highest possible liquidity for investors. Unlike typical legacy businesses that mature over time, increase available information pertaining to the business which eventually leads to a liquidity event such as an initial public offering, ICOs provide a liquidity event for promoters and investors alike at a very early stage in the lifecycle of the platform. Legacy businesses that experience liquidity events for promoters and institutional investors have been subject to reporting requirements under the federal securities laws, accounting standards, legal infrastructure requirements, among many other requirements for several years if not decades, before they can experience a liquidity event. Because of these requirements, the investing public gets significant assurances of the underlying business success of the entity which drives demand. Because ICOs take typically place at the beginning of the lifecycle of a crypto business/platform, ICOs investors typically invest – and the token exchange – on very limited information which increases volatility of the tokens and the entire cryptocurrency market. Accordingly, ICOs and cryptocurrencies are a much riskier investment. Their riskiness may, however, be offset by the near unlimited use cases for blockchain technology.

Open Source

Crypto businesses use typically open source code which creates risk factors not associated with legacy businesses. Most token offerings are based on open-source software. While it is possible to consider a token issuance with a closed system, such closed binary creates significant security concerns. By contrast, the open source code and all its features can be copied at any times. Accordingly, the utility of a token that was issued to investors can at any time be recreated in another token with the same or essentially the same features at marginal costs. Investors cannot rely on the implicit promise that the token promoters and their developers will increase the value of the acquired token and not create another token with identical features. Starting another token with the same features entails rather limited financial penalties. Moreover, if a given token offering was very successful, other promoters may have incentives to copy the token and its features. A concrete example of this risk is provided by Stellar. Stellar is in essence a copy of Ripple with almost identical features. While open-source crypto startups have licenses that help protect them from competitor companies who may be using their code for profit, legacy businesses that own their code and can sue competitors who copy such code which provides a different incentive structure and makes ICO investments riskier.

No Liquidity Preference

In the case of bankruptcy or termination of the promoter’s business / the platform token investors invested in, token holders typically do not have a liquidity preference. After the debt holders and outside creditors were satisfied with the liquidation value of the corporation, token holders typically have no recourse at all. By contrast, in a typical venture capital seed stage investment, the venture capital fund should typically obtain at least a simple liquidity preference, e.g. the venture capital fund typically will be able to reclaim their initial seed investment before other claims will be paid. Some venture capital funds can get more than their initial investment back, depending on the agreement and other factors they may obtain a 1.5 or 2 times liquidity preference. Again, by contrast, token holders typically lose everything they invested as they have no liquidity preference at all.

Legal Uncertainty

The lack of a regulatory framework creates significant legal uncertainty in the ICO market. Moreover, cryptocurrencies are censorship-resistant and arguably regulation-resistant by design, leading some to argue that regulatory uncertainty associated with coin offerings may sooner or later lead the Securities and Exchange Commission to declare ICOs illegal. Token valuation is also largely uncertain and subject to incalculable risks. ICOs are not subject to predefined regulatory procedures. Whitepapers do not follow prospectus disclosure guidelines, are not reviewed or unaudited by any authorities and are not subject to any forms of rating of the new entrepreneurial initiatives. To combat these shortcomings, a private initiative, a joint-venture between Ambisafe Inc. and the Russian-based rating agency ICOrating, has been created to ensure high-quality standards, supporting investors in their due-diligence and identify potential opportunities of investment in cryptocurrencies. The parameters to evaluate the entrepreneurial initiatives take into account different indicators, that span from economic and financial parameters to more technical elements. To provide support for crypto investors, companies like Deloitte and Price Waterhouse Coopers have built specific expertise in the identification of vulnerabilities within the code and the business model of startups. Identifying legitimate projects, distinguishing them from scams, is vital to pursue investors’ protection while creating the conditions for ICOs to proliferate. Bitcoin’s and Ethereum’s founding characteristics of decentralization, independence, openness and consensus based on proof of work provide a relatively easy way to identify scams.

2. Red Flags

Zombie ICOs are ICOs that really have little chance of creating a successful market for their tokens. Such ICOs have become increasingly common in 2017. Zombie ICOs often cannot succinctly answer core questions in their whitepaper or in response to questions by possible investors. Their inability to respond to legitimate questions often involves addressing issues such as the core business and infrastructure problem the investment proposition solves, allocation of ICO proceeds towards building the underlying product, most viable products or pre-production solution, availability of underlying assets. Moreover business plans of Zombie ICOs often cannot clearly articulate how the product of the respective company works or why the investing public and customers should care about it. Zombie ICOs teams also often do not have sufficient experience in starting and running a business. Finally, investors often do not obtain sufficient information for their investment decision in the respective ICO.

Core Problems with ICOs in 2017 can be narrowed down to several uniformly identified bad practices. First, ICOs that propose uncapped raises without an underlying product constitute a very serious red flag for any investor. Uncapped ICOs have several disadvantages. First, promoters who engage in uncapped raises are often perceived by the crypto community as greedy. Second, for crypto investors, uncapped ICOs raise the uncertainty for investors about the valuation of the underlying platform / product there are buying with their investment.

Because of such concerns, capped token issuances became the dominant structure between 2016 and 2017. As Vitalik Buterin emphasized, “capped sales have the property that it is very likely that interest is oversubscribed, and so there is a large incentive to getting in first.” Examples include the token issuances Blood and BAT. With regard to the former, an amount of tokens equal to $ 5.5 million was sold in two minutes, whereas in the latter $35 million were sold in 30 seconds. The Gnosis ICO ($ 12.5 million) was another landmark in the structural evolution of ICOs. To mitigate the inefficiencies and the risks of a capped sale, the Gnosis ICO was structured as a reverse dutch auction, i.e. not only the ICO was capped to $12.5 million, but in addition the time necessary to complete the sale impacted the quantity of tokens distributed among the investors, with the rest held by the start-up team.

ICO promoters should avoid several emerging bad ICO practices. Such practices include allowing tokens to be traded before underlying protocol network or application is live, using a landing page that focuses almost exclusively on the ICO with project timeline etc. but provides less content on product, project, technology, and team. Moreover, ICO promoters should include significant and ongoing disclosures on vesting and lockup periods, should never manipulate the smart contract to change ICO sales rules mid-course during the ICO. Moreover, the ICO disclosures have to be as clear as possible and should avoid an unclear or uncertain use of proceeds pie chart and should be very clear on cryptocurrency conversion plans into actual company reserves. Finally, ICO promoters should always disclose changes in company via 10k 10q 8k equivalence.

Conclusion

ICO practices will continue to evolve and improve the capital formation for crypto startups. Bad practices in ICOs will over time be curtailed via voluntary or imposed industry practices. Through ICOs’ evolution and continuous practice improvements, the ICO industry and underlying crypto businesses can become the foundation of the emerging crypto economy.